Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Why does Naval say: ZCash is an insurance policy for Bitcoin privacy?

Original Article Title: "Why Naval Says: ZCash is Bitcoin's Privacy Insurance?"

Original Article Author: Max Wong @IOSG

Introduction

Over the past few months, Zcash ($ZEC) has been in the spotlight, with Zcash surging from $47 to $292 in 30 days in September 2025, an increase of 620%. It has currently reached its highest price in 8 years at $429, pushing its Fully Diluted Valuation (FDV) over $8 billion.

In an era of increasing financial regulation, privacy-focused projects have once again become the focus of cryptocurrency. Therefore, Zcash (ZEC), as one of the pioneers of privacy coins, has once again piqued people's interest. This wave of enthusiasm has reignited people's interest in "freedom money," which is often used to describe private, censorship-resistant digital cash. Zcash, as a rapidly growing privacy coin, brings true financial privacy through encryption technology, expanding on Bitcoin's vision.

This report aims to delve into Zcash's technology and infrastructure, compare it to other privacy participants, and analyze the catalyst behind the recent resurgence of the Zcash ecosystem.

Zcash - What is it and How Does it Work?

Zcash is a privacy-focused digital currency launched in October 2016, forked from the Bitcoin codebase. It intentionally borrows many of Bitcoin's monetary principles; Zcash operates on a proof-of-work blockchain,

while also featuring the following:

· Fixed Supply: A limit of 21 million coins and a predictable halving schedule.

· Fair Emission: No premine, similar to Bitcoin's issuance model.

· Decentralization: Permissionless, no central authority, does not rely on intermediaries.

Privacy Standard

Zcash uses zk-SNARKs (Zero-Knowledge Succinct Non-Interactive Argument of Knowledge), which allows for transaction validation without revealing any details of the sender, receiver, or amount. In simple terms, Zcash provides users with fully encrypted transactions, masking on-chain data that Bitcoin's transparent ledger cannot achieve. In fact, this privacy mechanism of ZK is what Satoshi Nakamoto wanted to explore on Bitcoin but was not technically feasible at the time.

# Transaction Detail Encryption

When a user conducts a shielded transaction, key details such as the sender's address, recipient's address, and transaction amount are fully encrypted on the blockchain.

# Creating a ZK Proof

The sender (prover) uses their private key to generate a zk proof (zk-SNARK), confirming the satisfaction of several conditions, all without revealing sensitive data:

· The sender has sufficient funds to make the transaction.

· The spent funds were validly created in a previous transaction.

· The transaction input value equals the output value, preventing the generation of counterfeit coins.

· The sender is authorized to use the funds (has the correct private key).

· The funds have not been previously spent (using a mechanism called "nullifiers").

# Instant Verification

Other nodes on the Zcash network (verifiers) use public verification keys to instantly verify the zk-SNARK proof. The proof is very small (a few hundred bytes) and can be verified in milliseconds, making the verification process highly efficient.

Double-Spending Protection

It is important to note that Zcash's privacy is optional—users can remain transparent to meet compliance or auditing needs, or they can choose to be fully shielded.

ZEC uses a dual-address system, including transparent addresses (t addresses) and shielded addresses (z addresses). Transactions between transparent addresses are similar to any non-private blockchain transaction, but transactions involving shielded addresses are encrypted and private. When sending ZEC, the ledger will not display any information about the transacting parties or the value, only indicating a valid transaction has occurred. Only the participants (and those they choose to share an optional viewing key with) can see detailed information.

This feature gives Zcash fungibility (each unit is interchangeable), unaffected by past transaction history, thus achieving true financial privacy when using shielded transactions.

Three Main Funding Pools

The widespread implementation of shielded transactions is a significant technical challenge. Zcash has undergone three major upgrade iterations to enhance its encryption technology and efficiency:

#Sprout (2016)

--The initial release version--demonstrated that privacy based on zk-SNARKs is feasible on a public blockchain. However, Sprout transactions had a high computational cost (requiring several gigabytes of RAM, impractical on mobile devices) and relied on trusted setup (one-time parameter generation). Figures like Edward Snowden, using the alias "John-Doeb," participated in this notable setup to ensure no party could compromise the parameters. The traditional Sprout z addresses (typically starting with zc...) are now deprecated but still in use.

#Sapling (2018)

--A significant upgrade that greatly improved performance and usability. Sapling reduced proof times and memory requirements by over 100 times, ultimately making private ZEC transactions viable on everyday devices (even smartphones). It also introduced key features such as diversified addresses (allowing one key to have multiple shielded addresses, enhancing privacy) and viewing keys (enabling users to share read access to their transaction details for auditing or compliance purposes). Sapling still relies on a multiparty trusted setup but represents a significant step forward in practical private payments. Sapling z addresses (Bech32, zs...) are still supported, allowing users to transact with legacy tokens.

#Orchard (2022)

--The latest generation product, achieving trustless privacy. Orchard leverages the Halo 2 proof system (developed by Zcash engineers), requiring no new trusted setup. It further improves efficiency, supports batch transactions, and enhances synchronization, among other features. With Orchard, Zcash's privacy not only becomes stronger (without setup assumptions) but also more scalable—it aims to support future layer-two solutions like ZK-rollups. It also introduces Unified Addresses (UA, u1...), which can aggregate recipients of Orchard (and optionally Sapling + transparent) into one address; wallets typically default to routing new funds to Orchard. Thus, Orchard is now the default shielded pool for modern Zcash wallets.

A common summary of Zcash's development journey is: Sprout proved the possibility of private funds, Sapling made it usable, and Orchard made it trustless and scalable.

Upcoming Upgrades

Crosslink: Zcash's technical infrastructure is constantly evolving. The project is currently undergoing a significant upgrade called Crosslink, which will introduce a Hybrid Proof of Stake (PoS) layer on top of the existing Proof of Work consensus. This will allow ZEC holders to stake their coins to earn rewards and participate in finalizing blocks, while miners continue to produce blocks—combining the advantages of PoW and PoS. This hybrid approach is expected to improve network throughput and security (by providing quick finality and making 51% attacks more difficult).

Tachyon Project: Zcash developers (especially cryptographer Sean Bowe) are leading the implementation of the Tachyon project—aimed at significantly enhancing Zcash's shielded protocol scalability. The Tachyon project seeks to eliminate performance bottlenecks (such as every wallet having to download and scan every note) through innovative technologies like proof-carrying data, enabling "planetary-scale" private payments.

ZCash vs. Monero Comparison

Zcash (ZEC) positions itself as a Bitcoin-like currency but with optional encrypted privacy. Its shielded transfers use zk-SNARK, allowing validators to verify transaction correctness without seeing the sender, receiver, or amount. With Opt-in Audits (OA), wallets can send funds to the correct recipient while maintaining auditability: users can still transparently transact or share a viewing key with auditors/regulators. The outcome is user choice; when actively using the shielded pool, privacy is strongest.

Monero (XMR) utilizes a different toolkit, providing privacy by default in each transaction: Ring Signatures (mixing the original transaction with many decoy transactions so observers cannot discern which wallet truly sent the funds), RingCT (hiding amounts), and Stealth Addresses (receivers obtain payment at a one-time hidden address, which cannot be linked back to their real wallets). This makes usability straightforward but privacy is probabilistic: strength depends on ring size (e.g., 16), decoy choice, and user behavior. In practice, its privacy is high but lacks opt-in disclosure for audits, and due to compliance friction, some exchanges avoid listing it.

In general: Ring signature achieves transaction anonymity by placing the transaction among multiple decoy transactions (one could say Monero just added plausible deniability), while zk-SNARK proves the validity of a statement without revealing any information beyond the validity of the statement itself. Initially, people were hesitant about ZCash due to the need for a trusted setup. However, with the recent introduction of the Halo upgrade, ZCash can generate zk-SNARKs without requiring a trusted setup. Despite many challenges, the Monero traceability heuristic paper has shown that Monero has some form of traceability through "Wallet App Bugs and Mordinal-P2Pool Perspective."

So, why did the market choose ZCash?

What Happened?

Over the past two months, from early September to now, $ZEC has been on a continuous upward trend, starting from ~$40 to ~$429, a growth of over 1000%. What was the catalyst for this surge? What are the reasons behind it?

Introduction of Zashi

One of the significant contributors to ZCash's recent growth is the Electric Coin Co's (ECC) focus on consumers. Previously, the protocol focused primarily on ZCash's core - establishing cryptography and technology. Now, they are more focused on user experience and user onboarding. A significant part of this work has been the development of Zashi, the official ZCash wallet.

Josh Swihart - ECC CEO:

"When I took over as CEO of ECC in February 2024, we decided to truly focus on user experience... We built a wallet called Zashi. After Zashi was launched, you could see an exponential increase in shielded transaction totals and the ZEC amount in the shielded pool."

The launch of Zashi significantly improved the usability of ZCash. It provides a sleek interface comparable to popular EVM wallets, supports features such as view keys, hardware wallet integration, and plans to enable shielded watchtower and staking post-launch. More importantly, Zashi is designed specifically for shielded ZEC transactions, meaning all transactions sent using Zashi are private by default. If a user receives transparent ZEC, the wallet prompts you to shield it before spending. Additionally, Zashi supports single-address multisource from all different pools (Sprout, Sapling, Orchard), allowing users to seamlessly migrate funds between different pools.

Compared to a few years ago, this is a significant change, as back then, privately using Zcash required using multiple dedicated software across different products. Due to these breakthroughs in user experience, the adoption of shielded pools has grown exponentially, indicating that many users would indeed opt for privacy if there was a convenient option.

By making private transactions simple, just a few taps away, and abstracting the technical complexity, these wallets have driven the adoption by users with lower technical expertise. The improvement in wallet user experience is considered a primary driver of ZCash's recent growth.

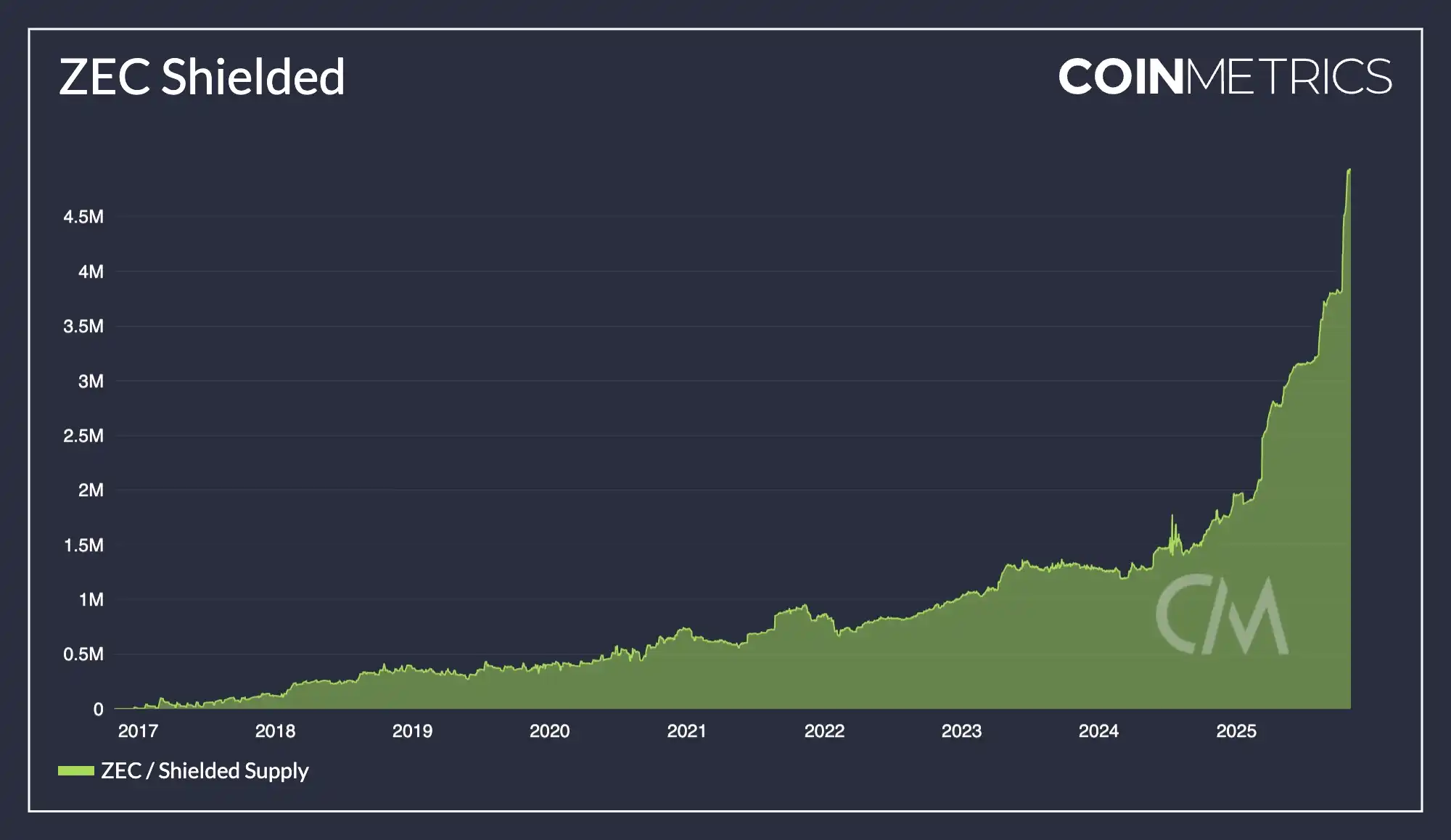

One of the most significant signs of Zashi's contribution to the Zcash ecosystem's momentum is the explosive growth in on-chain shielded usage. As of the fourth quarter of 2025, over 4.5 million ZEC is stored in shielded addresses, accounting for approximately 28% of the total supply. This is a record-breaking high, while a few years ago, this ratio was only 5%. The graph above illustrates how the shielded pool began to grow exponentially around 2024, directly coinciding with the release of Zashi.

This means that more ZEC has entered Zcash's shielded pool, which, in turn, enhances the network's privacy for everyone (a larger anonymity set). In practice, this also tightens the liquidity in circulation (as shielded funds are harder to trace and are often held long-term to protect privacy), thus having a positive impact on price dynamics.

Introducing NEAR Intents - Crosspay

Zashi's CrossPay also serves as Zcash's large-scale onboarding mechanism, fundamentally achieving interoperability within the Zcash ecosystem.

Crosspay is a cross-chain bridging/exchange solution that leverages NEAR Intents, allowing users to swap in and out of ZEC from another chain while still preserving privacy; Zashi also harnesses NEAR for decentralized off-chain, enabling users to swap from ZEC to another chain (or to a fiat gateway) without revealing their ZEC address—completely eliminating the need for CEX. This has driven a significant influx of capital and users into the ZEC ecosystem.

NEAR Intents is a chain-agnostic protocol: users (or agents) state what they want (e.g., "swap BTC→ZEC" or "pay 50 USDC to this address"), and a decentralized network of resolvers competes cross-chain to execute; users only need to sign one approval. It abstracts the bridge/DEX hops and optimal price/liquidity routes.

· User requests "Swap X → ZEC" or "Pay Y USDC on Z chain".

· NEAR Intents Resolver competes to return the best quote.

· User approves once in Zashi; Resolver executes cross-chain route; ZEC is shielded or recipient receives the exact token.

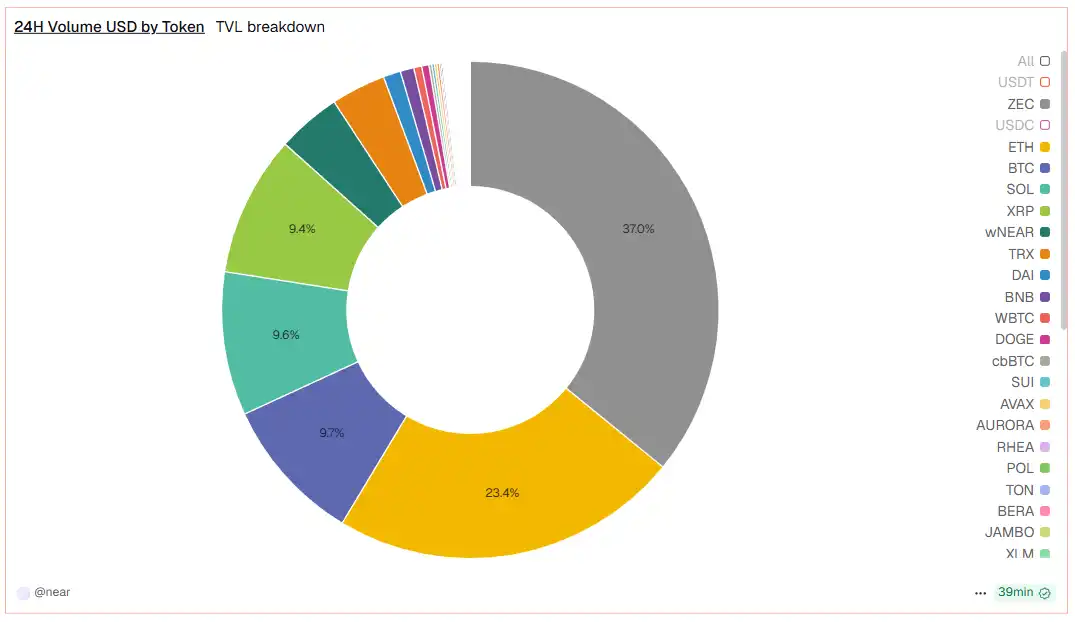

Exclude USDC and USDT amounts from this sample; currently, ZEC NEAR Intent amount represents over 30% of the NEAR Intent total.

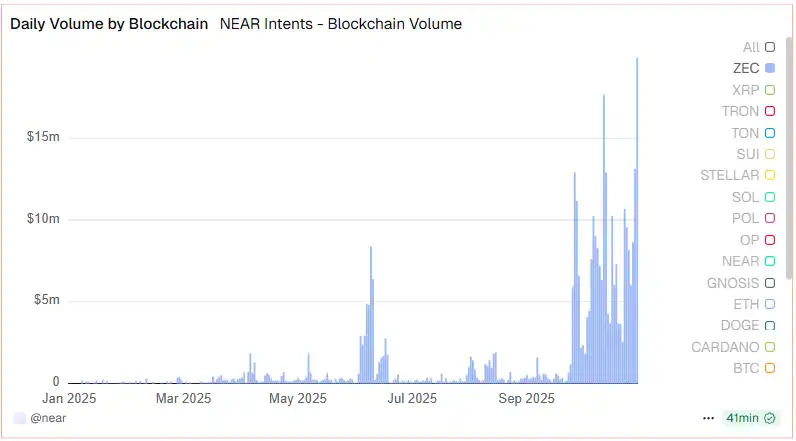

Overall, we can infer that the integration of Zashi with Crosspay is also a major driver of market share growth, with the magnitude of ZEC NEAR Intent set to increase significantly starting from September 2025, coinciding with the launch of Crosspay.

The New Significance of Double Transaction Type Privacy — A Story

As governments and regulatory bodies around the world intensify monitoring measures (from stricter KYC/AML to tracking central bank digital currencies), the cypherpunk ethos is once again in focus. Zcash provides a refuge for those concerned about these trends: a form of encrypted, untrackable currency.

"They only care about the digital rise, not noticing the fall of freedom."

As mainstream cryptocurrency users realize that privacy is being eroded (e.g., Tornado Cash and other mixer currencies being blacklisted), many are turning to on-chain privacy alternatives. Zcash stands out as a battle-tested L1, with its privacy-preserving capabilities stronger than mixer protocols (reportedly, Zcash has a broader use case than Tornado Cash).

In short, the rise of the "freedom narrative" has shaped Zcash into a key asset for upholding financial liberty — a narrative that resonates with both ideological investors and those purely seeking to hedge against "Big Brother".

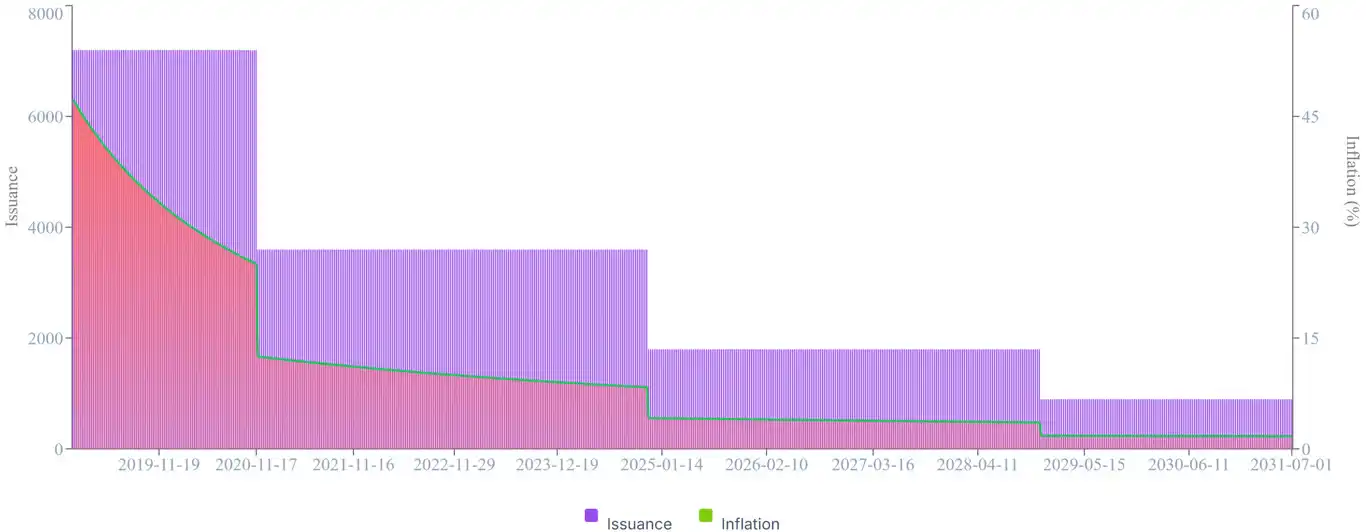

Post-Halving Supply Dynamics

The second halving of Zcash (November 2024) significantly reduced its new coin issuance, and we are now seeing its impact. The block reward dropped from 3.125 ZEC to 1.5625 ZEC, cutting the annual inflation rate in half. Historically, Bitcoin's price didn't sustainably exceed $1000 until after the second halving—after which Bitcoin's price surged parabolically. Zcash's supply curve is identical to Bitcoin's, just shifted by a few years, and has just crossed the same milestone.

▲ ZEC USD Issuance and Inflation Schedule

While demand is rising, the circulating supply is tightening, creating the typical supply-demand squeeze. Investors speculate that, with the high-inflation 'suspense' gone, ZEC may follow the early Bitcoin trajectory. In fact, by the fourth quarter of 2025, ZEC's market performance has already outpaced most major coins. Some of this may be mere market timing, but fundamentally, Zcash's tokenomics are becoming increasingly appealing as it matures: it has a fixed cap, continuously decreasing emissions, and the end of miner rewards is approaching, akin to Bitcoin's development path.

▲ ZEC USD Price and Halving Schedule

The notion of halving—though misunderstood by some traders (the rumor of a 2025 halving is false)—still drew attention to the Zcash narrative.

You may also like

After two years, Hong Kong's first batch of stablecoin licenses finally issued: HSBC, Standard Chartered make the cut

The person who helped TAO rise by 90% has now single-handedly crashed the price again today

3-Minute Guide to Participating in the SpaceX IPO on Bitget

Top 5 Cryptos to Buy in 2026 Q1: A ChatGPT Deep Dive Analysis

Explore the top 5 cryptos to buy in Q1 2026 including BTC, ETH, SOL, TAO, and ONDO. See price outlooks, key narratives, and institutional catalysts shaping the next market move.

How to Earn $15,000 with Idle USDT Before Altcoin Season 2026

Wondering if altcoin season is coming in 2026? Get the latest market update, and learn how to turn your idle stablecoins waiting for entry into extra rewards up to 15,000 USDT.

Can You Win Joker Returns Without Large Trading Volume? 5 Mistakes New Players Make In WEEX Joker Returns Season 2

Can small traders win WEEX Joker Returns 2026 without huge volume? Yes—if you avoid these 5 costly mistakes. Learn how to maximize card draws, use Jokers wisely, and turn small deposits into 15,000 USDT rewards.

Altcoin Season 2026: 4 Stages to Profit (Before the Crowd FOMO In)

Altcoin Season 2026 is starting — discover the 4 key stages of capital rotation (from ETH to PEPE) and how to position before the peak. Learn which tokens will lead each phase and avoid missing the rally.

Will Alt season come in 2026? 5 Tips to Spot the Next 100x Crypto Opportunities

Will altcoin season arrive in 2026? Discover 5 rotation stages, early signals smart traders watch, and the key crypto sectors where the next 100x altcoin opportunities may emerge.

The bear market has arrived, and cryptocurrency ETF issuers are also getting involved

The richest man had a quarrel with his former boss

BTC Firm Above 70K! Saylor’s "Institutional Logic" vs. Moon’s "Retail Faith": Who is Really Harvesting the Market?

Bitcoin is holding firm above the $70,000 support level following a massive short squeeze that liquidated $427 million. As the "Four-Year Cycle" narrative shifts, the market is split: Michael Saylor’s cold, institutional "indiscriminate stacking" vs. Carl Moon’s high-energy retail "hopium." This article decodes these two polar-opposite strategies for the 2026 bull run and reveals how WEEX’s institutional-grade liquidity and AI trading tools empower every type of investor to convert market volatility into profit.

The Girl Who Created the SBTI Test: A Story of a Doomed Cyber Love, an E-Widow Ratfolk

B.AI Officially Launched: Building AI Agent Financial Bedrock Platform, Driving AGI Era Business Underlying Logic

B.AI Officially Launched: Breaking Down A2A Collaboration Barriers to Unlock the Smart Body Economy's Full Potential

We helped Xu Mingxing write a book called "<OK Life>".

Rare APY of 400%, is TradeXYZ handing out money to oil bulls?

a16z: Perpetual Contracts are Rewriting Global Trading Rules

Bitcoin Hits $73,000 Triggering $427M Short Liquidation | Carl Moon: $200,000 is the Target

April 9, 2026 (UTC+0), 22:17. Bitcoin (BTC) executed a high-velocity surge within minutes, heavy-hitting the $73,000 psychological barrier and touching a local high near $74,000. While the price has since retraced to consolidate above $72,000, this "instant ambush" successfully completed a $427M liquidation of short positions.

After two years, Hong Kong's first batch of stablecoin licenses finally issued: HSBC, Standard Chartered make the cut

The person who helped TAO rise by 90% has now single-handedly crashed the price again today

3-Minute Guide to Participating in the SpaceX IPO on Bitget

Top 5 Cryptos to Buy in 2026 Q1: A ChatGPT Deep Dive Analysis

Explore the top 5 cryptos to buy in Q1 2026 including BTC, ETH, SOL, TAO, and ONDO. See price outlooks, key narratives, and institutional catalysts shaping the next market move.

How to Earn $15,000 with Idle USDT Before Altcoin Season 2026

Wondering if altcoin season is coming in 2026? Get the latest market update, and learn how to turn your idle stablecoins waiting for entry into extra rewards up to 15,000 USDT.

Can You Win Joker Returns Without Large Trading Volume? 5 Mistakes New Players Make In WEEX Joker Returns Season 2

Can small traders win WEEX Joker Returns 2026 without huge volume? Yes—if you avoid these 5 costly mistakes. Learn how to maximize card draws, use Jokers wisely, and turn small deposits into 15,000 USDT rewards.